4h ago

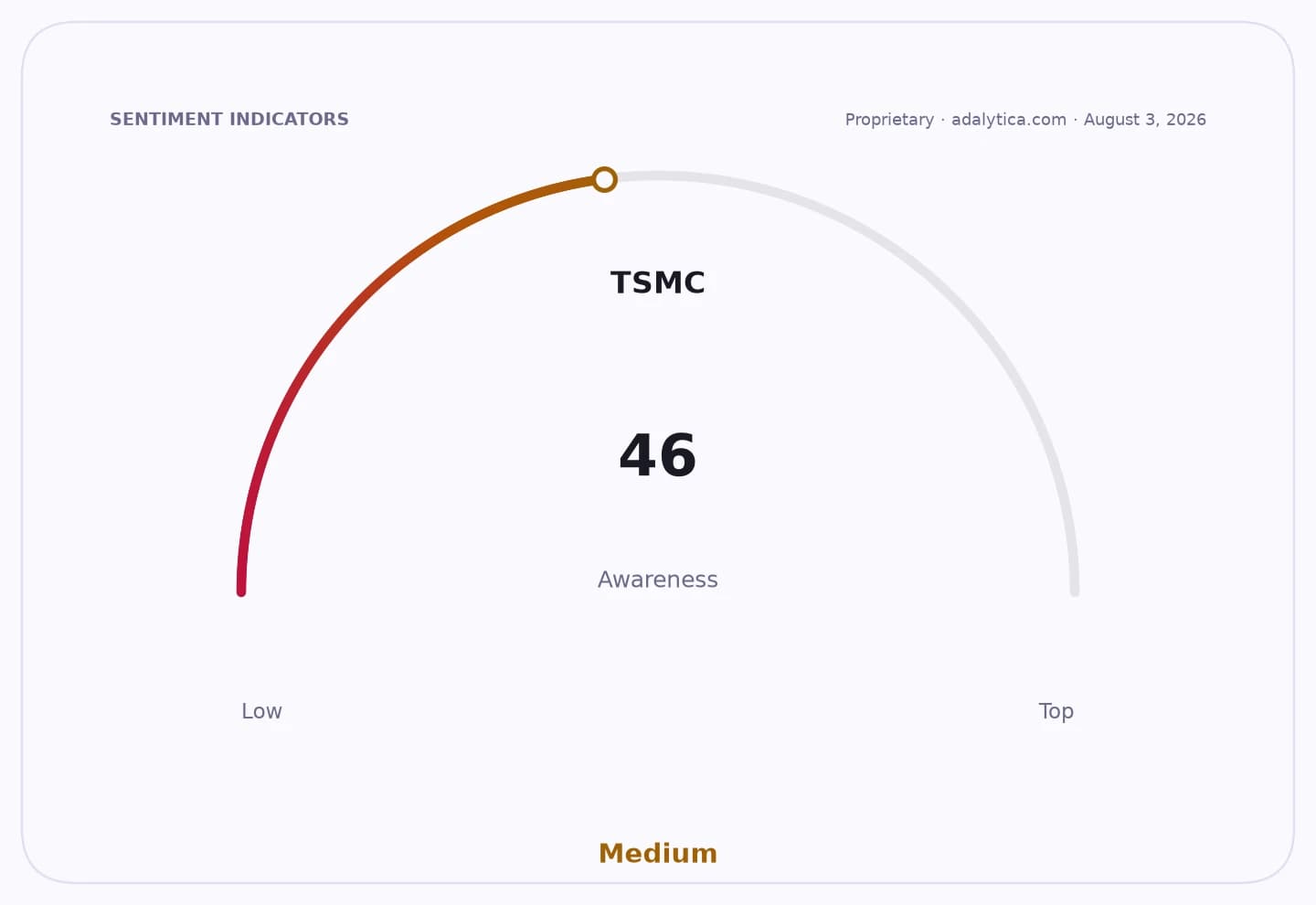

TSMC Q2 2026: AI Drives Records but Peak-Margin Risk Emerges

TSMC posted record revenue with net profit surging 77.4% year-on-year in Q2 2026. AI chips now make up 66% of quarterly revenue, underscoring sustained demand. Yet the results also flag peak-margin risk even as AI growth accelerates.